What Is a 401(k) and How Does It Work? Complete 2026 Guide

A 401(k) is the most powerful retirement savings tool available to American workers. In 2026, you can stash up to $24,500 tax-deferred — and your employer may match part of it for free. Here's everything you need to know.

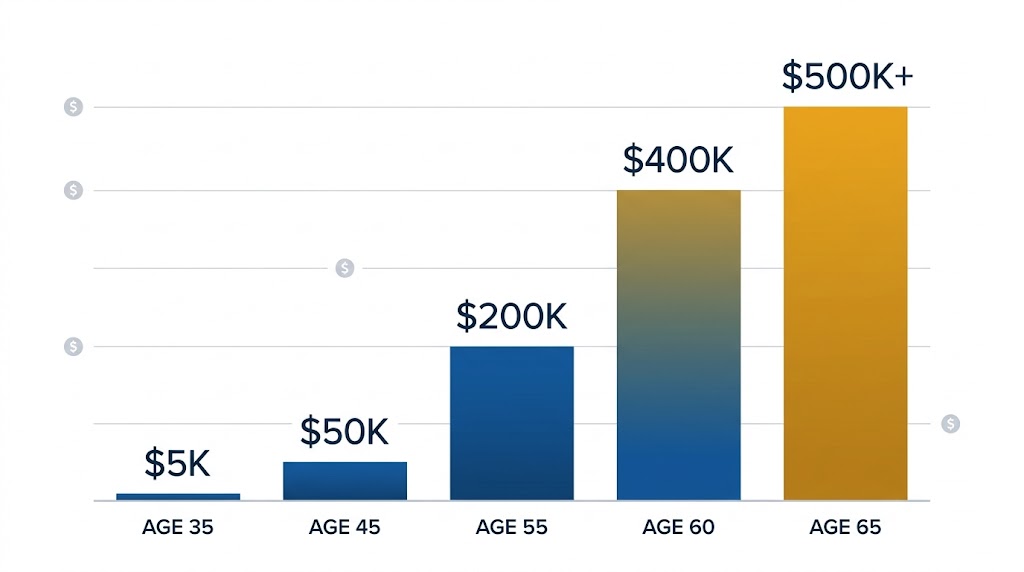

See exactly how much your 401(k) will be worth at retirement with our free 401(k) calculator — includes employer match, 2026 IRS limits, and inflation adjustment.

What Is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan authorized under Section 401(k) of the Internal Revenue Code. It allows employees to contribute a portion of their pre-tax paycheck into a tax-advantaged investment account. Your contributions reduce your taxable income today, and your investments grow tax-deferred until you withdraw them in retirement.

Named after the tax code section that created it, 401(k) plans were introduced in the late 1970s as a supplement to traditional pensions. Today, they are the primary retirement savings vehicle for most American workers — with over 70 million active participants according to the Investment Company Institute.

How Does a 401(k) Work?

When you enroll in your employer's 401(k), you choose what percentage of each paycheck to contribute. That money is deducted before taxes are calculated, immediately reducing your take-home pay by less than your contribution amount. For example, contributing $300/paycheck might only reduce your take-home by $225 if you're in the 25% tax bracket.

Your contributions are then invested in mutual funds, index funds, or target-date funds within the plan. These investments grow tax-free until withdrawal.

2026 IRS Contribution Limits

| Participant | 2026 Limit | Change from 2025 |

|---|---|---|

| Under age 50 | $24,500 | +$1,000 |

| Age 50+ (catch-up) | $32,500 | +$1,000 |

| Total (employer + employee) | $70,000 | +$2,000 |

Source: IRS Notice 2025-XX. Limits are indexed to inflation annually.

Employer Matching — Free Money

Many employers match a portion of your 401(k) contributions. A common structure is 50% match up to 6% of salary. If you earn $70,000 and contribute 6% ($4,200), your employer adds $2,100 — an immediate 50% return on that portion of your savings.

Not capturing the full employer match is one of the most costly financial mistakes workers make. Prioritize contributing at least up to the match before any other investment.

Traditional vs. Roth 401(k)

Many plans now offer both options:

- Traditional 401(k): Contributions are pre-tax. You pay taxes when you withdraw in retirement. Best if you expect to be in a lower tax bracket later.

- Roth 401(k): Contributions are after-tax. Withdrawals in retirement are completely tax-free — including all investment gains. Best if you expect to be in a higher tax bracket in retirement.

Most financial advisors recommend contributing to a Roth option if you're early in your career, as tax-free compound growth over 30+ years is enormously valuable.

What Happens to Your 401(k) If You Leave Your Job?

When you leave an employer, you have four options for your 401(k):

- Roll it over to your new employer's plan

- Roll it over to an IRA (Individual Retirement Account)

- Leave it with your former employer (if allowed)

- Cash it out (subject to income taxes + 10% penalty if under 59½)

Rolling over to an IRA typically gives you the most investment options and lowest fees. Cashing out should almost always be avoided due to the tax penalty.

How to Maximize Your 401(k)

- Contribute at least enough to get the full employer match — always

- Increase your contribution by 1% each year (or use auto-escalation)

- Choose low-cost index funds (look for expense ratios below 0.20%)

- Use target-date funds for automatic age-appropriate allocation

- Rebalance once per year to maintain your target allocation

Use our free 401(k) calculator to see exactly how much your contributions will grow by retirement — with employer match, 2026 IRS limits, and inflation adjustment included.

Frequently Asked Questions

IRS Publication 560 (Retirement Plans for Small Business) · Investment Company Institute 401(k) Data 2025 · SECURE 2.0 Act of 2022 · IRS Notice 2025 (2026 Contribution Limits) · U.S. Department of Labor Employee Benefits Security Administration