How Inflation Affects Your Savings (And How to Fight Back) 2026

Inflation is a silent tax on your savings. Every year prices rise, your money buys less — even while the balance number in your account stays the same. Here's exactly how much you're losing, and what to do about it.

See exactly how much purchasing power any dollar amount loses over time.

Inflation Calculator →The Real Cost of Inflation on Savings

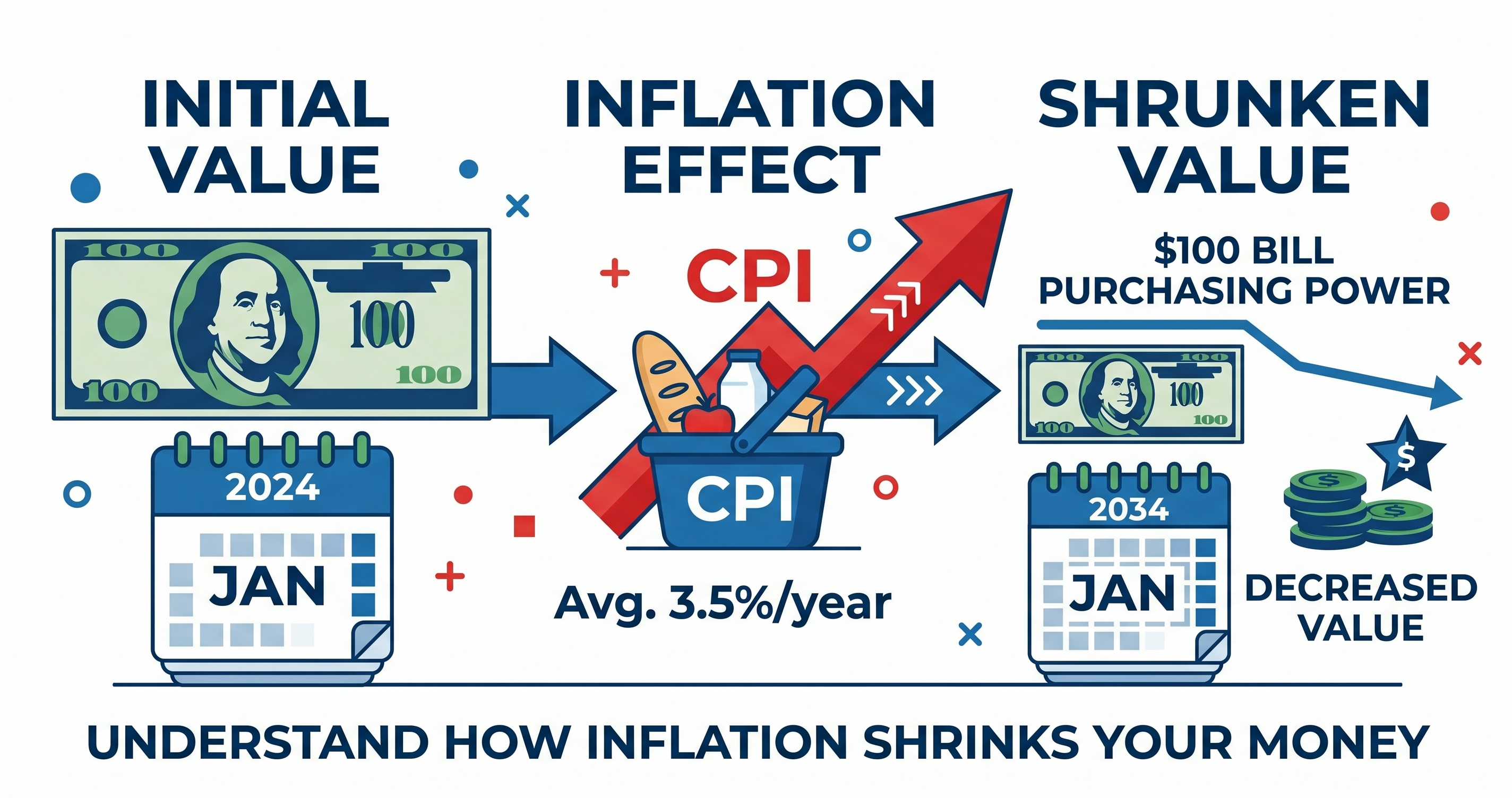

Inflation doesn't appear as a line item on your bank statement — but it's constantly reducing what your savings can buy. At 3% annual inflation, here's what happens to $100,000 over time:

| Years | At 2% Inflation | At 3% Inflation | At 5% Inflation |

|---|---|---|---|

| 5 years | $90,573 | $85,873 | $78,353 |

| 10 years | $81,707 | $74,409 | $61,391 |

| 20 years | $67,297 | $55,368 | $37,689 |

| 30 years | $55,207 | $41,199 | $23,138 |

Starting $100,000 in a savings account at 0.5% interest while inflation runs at 3% means you lose approximately $2,500 in real purchasing power every year — the bank says you have more, but you can buy less.

What Is the Current US Inflation Rate? (2026)

US inflation (CPI) was approximately 2.4%–2.9% in early 2026, down significantly from the June 2022 peak of 9.1% — the highest since 1981. The Federal Reserve targets 2% annual inflation as the ideal rate for economic stability.

At the current ~2.5% rate, $100,000 loses about $2,500 in real purchasing power each year — less severe than 2022 but still meaningful over decades. Source: US Bureau of Labor Statistics, BLS.gov.

5 Ways to Protect Your Savings From Inflation

1. Stock Market Index Funds (Best Long-Term)

The S&P 500 has historically returned ~10% per year before inflation, or ~7% after inflation. Over time, no other broadly accessible investment class has matched this. A $100,000 investment at 7% real return grows to $387,000 in 20 years in real purchasing power — vs. the same amount losing 45% in a 0.5% savings account. Use low-cost index funds (expense ratio below 0.1%) like Vanguard, Fidelity, or iShares S&P 500 funds.

2. I-Bonds (Best Inflation-Guaranteed Option)

US Treasury I-Bonds pay a fixed rate plus the current CPI inflation rate — guaranteeing you match inflation on that portion of savings. In 2022, I-Bonds briefly paid 9.62% when inflation peaked. Maximum purchase: $10,000/year per person directly from TreasuryDirect.gov.

3. TIPS (Treasury Inflation-Protected Securities)

TIPS are US government bonds whose principal automatically adjusts with CPI. If inflation rises 3%, your principal grows 3%. Available through TreasuryDirect or via TIPS ETFs for easy access. Lower return ceiling than stocks, but government-backed and inflation-proof.

4. High-Yield Savings or CDs (When Rates Beat Inflation)

High-yield savings accounts and CDs are only inflation-protective when their rate exceeds the current inflation rate. In 2023–2024, many online HYSA rates reached 5%+ when inflation was ~3–4% — a rare window of real positive returns on cash. In 2026, compare current HYSA rates to current CPI before relying on this strategy.

5. Real Estate

Real estate (particularly your primary home) historically appreciates at or slightly above inflation. Home values rose ~40% from 2020–2023, well above the ~17% cumulative inflation in that period. Real estate also provides rental income and mortgage leverage that can amplify real returns, though with higher complexity and illiquidity than financial assets.