What Is Debt-to-Income Ratio? How to Calculate Your DTI (2026)

Your debt-to-income ratio (DTI) is the single most important number lenders check when you apply for a mortgage or major loan — even more than your credit score in many cases. Here's exactly what it is, how to calculate it, and what counts as a good DTI in 2026.

Enter your debts and income — get your ratio, a visual meter, and lender verdict in seconds.

Free DTI Calculator →What Is Debt-to-Income Ratio (DTI)?

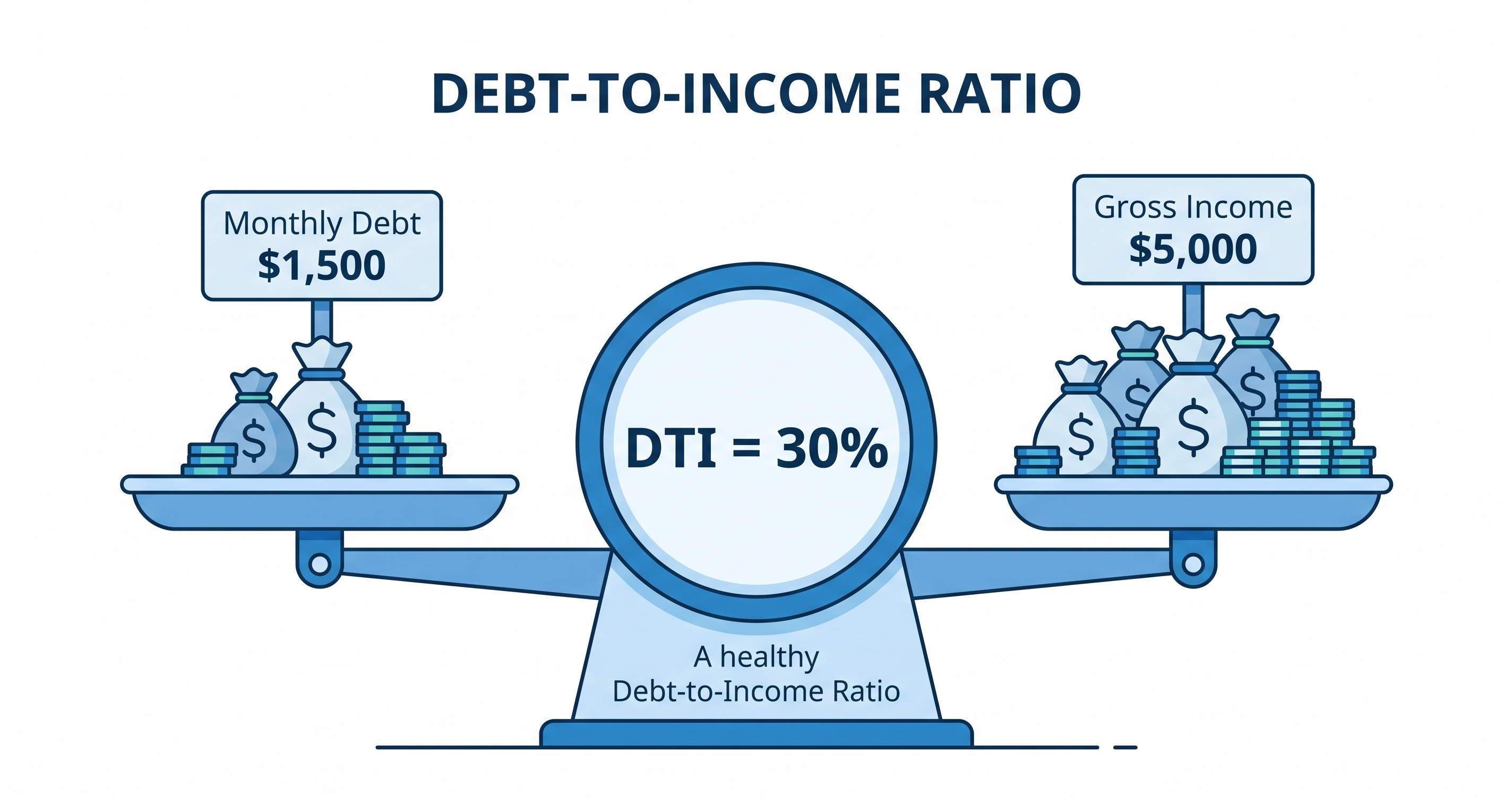

Debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward paying your monthly debt obligations. It is calculated by dividing your total monthly debt payments by your gross monthly income and multiplying by 100.

DTI Formula: (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

For example: if you pay $1,500/month in debts and earn $5,000/month gross, your DTI is 30% — which lenders consider good.

Lenders use DTI because it measures your actual ability to take on more debt, not just your history of paying it. Two people can have identical credit scores but very different DTIs — and the one with the lower DTI is the less risky borrower.

How to Calculate Your Debt-to-Income Ratio: Step by Step

Step 1 — Add Up All Monthly Debt Payments

Include every required monthly debt payment:

- Rent or current mortgage payment (including property tax and insurance)

- Car loan payments

- Student loan minimum payments

- Credit card minimum payments (not your full balance)

- Personal loan payments

- Child support or alimony obligations

- Any other recurring debt with a fixed monthly obligation

Do NOT include: utilities, groceries, gas, health insurance, subscriptions, or other living expenses — only actual debt payments with a formal obligation.

Step 2 — Find Your Gross Monthly Income

Use your gross income — before taxes and deductions, not your take-home pay. Include all sources: salary, freelance income, rental income, alimony received, Social Security, etc.

If you're salaried: Annual Salary ÷ 12 = Gross Monthly Income. ($60,000/year ÷ 12 = $5,000/month)

If you're hourly: Hourly Rate × Average Weekly Hours × 52 ÷ 12. ($25/hr × 40hrs × 52 ÷ 12 = $4,333/month)

Step 3 — Divide and Multiply

DTI = (Total Monthly Debts ÷ Gross Monthly Income) × 100

Rent: $1,200 + Car: $350 + Student Loan: $200 + Credit Card minimum: $100 = $1,850 total debt

Gross Income: $5,000/month

DTI = ($1,850 ÷ $5,000) × 100 = 37%

Or use our free DTI Calculator — enter each debt separately and get your ratio instantly.

What Is a Good DTI Ratio in 2026?

Here's how lenders interpret different DTI ranges:

| DTI Range | Rating | What Lenders Think |

|---|---|---|

| Below 20% | Excellent | Best rates, instant approval on any loan type |

| 20% – 35% | Good | Approved for most loans, competitive interest rates |

| 36% – 43% | Acceptable | Mortgage possible, may need strong credit score to offset |

| 44% – 49% | High | FHA loan possible, personal loans harder, higher rates |

| 50%+ | Too High | Most lenders will decline — reduce debt first |

Front-End vs. Back-End DTI — What's the Difference?

Mortgage lenders actually calculate two separate DTI ratios:

Front-End DTI (Housing Ratio): Only your proposed housing costs (mortgage principal + interest + property taxes + homeowner's insurance = PITI) divided by gross income. Most lenders want this below 28%.

Back-End DTI (Total Debt Ratio): ALL monthly debts (housing + car + student loans + credit cards + everything else) divided by gross income. Most lenders want this below 43%.

When people say "my DTI is 37%," they usually mean back-end DTI. That's also what our calculator measures. The general DTI guidelines (the 36% rule, the 43% mortgage limit) refer to back-end DTI.

DTI Requirements by Loan Type (2026)

| Loan Type | Max Front-End DTI | Max Back-End DTI | Notes |

|---|---|---|---|

| Conventional Mortgage | 28% | 43–45% | Fannie Mae allows 45% with strong credit |

| FHA Loan | 31% | 43–50% | More flexible; 50% allowed with compensating factors |

| VA Loan | No limit | 41% | Residual income also evaluated |

| USDA Loan | 29% | 41% | Rural properties only |

| Personal Loan | N/A | 43% | Varies significantly by lender |

| Auto Loan | N/A | 50% | Less strict than mortgage lenders |

Source: Fannie Mae, FHA guidelines, VA guidelines, USDA Rural Development (2026).

5 Ways to Lower Your DTI Ratio

Since DTI = Debt ÷ Income, you can lower it by reducing debt, increasing income, or both:

- Pay off small balances entirely — eliminating a $150/month car payment completely reduces your DTI more than making extra principal payments on a large loan. Target the smallest balances first for the fastest DTI improvement.

- Pay down credit card balances — credit card minimum payments are calculated as a percentage of your balance (typically 1–2%). Paying down a $5,000 card from $5,000 to $1,000 reduces your minimum payment from ~$100 to ~$20 — saving $80/month from your DTI calculation.

- Increase your gross income — a second job, freelance work, or raise directly increases the denominator. Even $500/month in additional gross income on a $5,000 base improves your DTI from 37% to 34.3% (using the $1,850 example above).

- Avoid new debt before applying — don't take on a car loan, new credit card, or any new financed purchase in the 3–6 months before a mortgage or major loan application. New monthly payments directly raise your DTI.

- Refinance existing loans — if interest rates have dropped since you took out a loan, refinancing to a lower rate reduces your monthly payment and therefore your DTI, even on the same balance.